Last Updated on March 11, 2024 by admin

Target and Actual of Production Orders

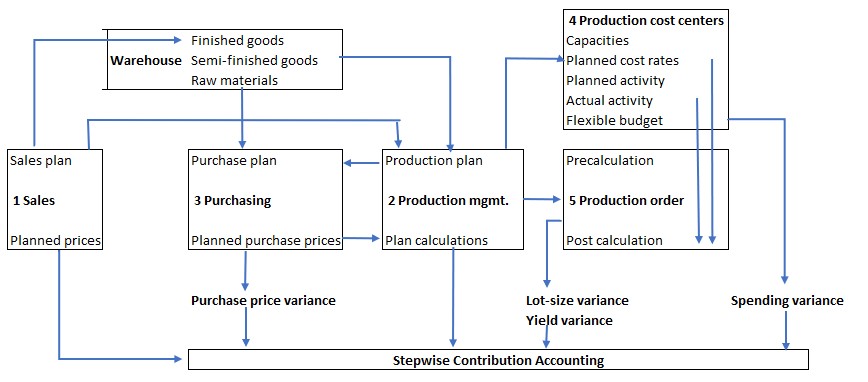

Product costing follows the planning and control process of a company:

-

- In sales, the quantity-based annual sales plan is drawn up per finished item, be it a physical product or a service unit.

- Production management determines the quantities to be produced per item on the basis of the sales plan. In doing so, it takes into account the existing inventory, the machine and personnel capacities of the production cost centers as well as expected interruption times due to vacations, public holidays and machine maintenance. Production management wants to have enough semi-finished products in inventory at all times in order to deliver the units sold on time and still manage with minimum average inventory levels. Therefore, production management must determine the lot sizes of the individual production orders.

- Purchasing ensures that the material requirements resulting from production and sales planning are available in stock on time. In addition, it negotiates with the potential suppliers in good time the planned purchase prices of the products and services to be bought. This is necessary to calculate the planned costs of the products and services.

- The managers of the manufacturing cost centers prepare the planning of their cost center on the basis of the planned activities resulting from the production plan. To do this, they need the planned production quantities, the standard times from the work plans for the items they produce and the setup-times to be scheduled for each production order. With this information they determine the planned activity of their cost center, i.e. the activity that is to be performed directly for the production orders to be processed.In the next step, the cost center managers consider how much auxiliary or operating materials will be required from the warehouse or directly from the suppliers in order to be able to perform the planned activity. They also plan which services will have to be procured from internal auxiliary cost centers (e.g. energy, water, compressed air, repairs and maintenance) depending on the planned employment.

The sum of these planned costs is divided by the planned activity, which results in the proportional planned cost rate of the cost center. This rate is used for the calculation of proportional product costs in planning as well as in actual (5). This data can be used to calculate the planned proportional (standard) costs of an item and the precalculation of a real production order. If these are deducted fromnet sales, the contribution margin I per product and summarized per product or customer group can be calculated, also in planned and actual data.

The precalculations of the orders of a month are decisive for the calculation of the monthly flexible budgets of the production cost centers. If the actual costs deviate from the flexible budget, consumption variances arise (per cost element). The cost center manager is responsible for these. He must ensure that corrections are made so that the company can achieve its profit targets.

See also “Management Control with Integrated Planning“, Chapters 4 and 5.

Wow, amazing blog layout! How long have you been blogging for? you made blogging look easy. The overall look of your web site is magnificent, as well as the content!

Hello Rachel, Thanks for the flowers. I hope the information helps.

Thanks, I have recently been looking for info about this subject for a while and yours is the greatest I have discovered so far. However, what in regards to the bottom line? Are you certain in regards to the supply?

Hello Eileen

Thank you for your comment. In management accounting we want to show for what the respective manager can be responsible. This is long before we come to the bottom line of the company. There it is to late to react because managers should intervene immediately in their own cost center.