If private individuals want to buy a new car, they first determine how much they will have to pay for the desired vehicle including all equipment features. This results in the gross purchase price of the vehicle, which is then also shown in the purchase contract. If her used car is traded in, the trade-in price is deducted. She may prefer a leasing contract with monthly payments. When making the decision, the private individual mainly considers the cash outflows at the time of purchase and the ongoing annual expenses. Such an investment calculation only takes cash flows into account.

Why write off?

A company, on the other hand, must present a financial statement with a profit and loss account every year. To determine the annual profit for the period, it must deduct the annual loss in value of the car, i.e. depreciation, from the revenue generated and show it in the income statement and in the balance sheet.

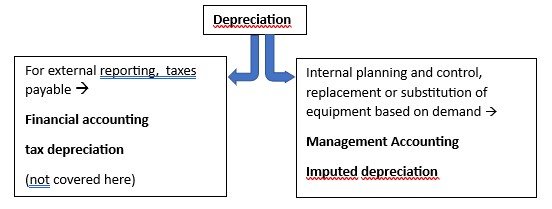

Depreciation is the value-based expression of the annual loss in value of physical and intangible assets. External reporting and the calculation of taxes payable are governed by legal regulations. These regulations are intended to ensure that all taxable companies report according to the same rules and are therefore treated equally by the state. The management approach, on the other hand, focuses on the loss in value of an asset or right due to its use and the expected remaining useful life of it. These different purposes can lead to different depreciation amounts being included from an operational perspective than those permitted under tax law.

External or internal valuation

In order to treat all their taxable companies equally, many countries issue commercial and tax regulations on the valuation of assets, the depreciation methods to be applied and the useful lives permitted for the calculation. In Germany, for example, these are the depreciation rules (depreciation for wear and tear), cf. the depreciation table of the German Federal Ministry of Finance (Bundesfinanzministerium – AfA-Tabelle für die allgemein verwendbaren Anlagegüter (AfA-Tabelle “AV”)). For internationally operating and reporting companies, the rules of international reporting standards such as IFRS or US GAAP are applied.

For the managers controlling a company or a group these external valuation and depreciation rules are of secondary importance. They want to be able to assess whether the depreciation and amortization charged to the internal financial statements will be sufficient to maintain the company’s performance potential in the future so that it can continue to generate profits in line with the market. Distributions (dividends) to owners and shareholders should therefore only be decided once it has been ensured by means of imputed depreciation and amortization that funds that will be required to maintain the profit potential will not be distributed.

“Management control plans, controls and measures the implementation of guidelines, strategies and operational objectives, see the management control definition.

From this understanding of management control it can be deduced that management accounting must take into account imputed depreciation, not financial depreciation. This is because it is about shaping the future of the company and only to a limited extent about external profit reporting.

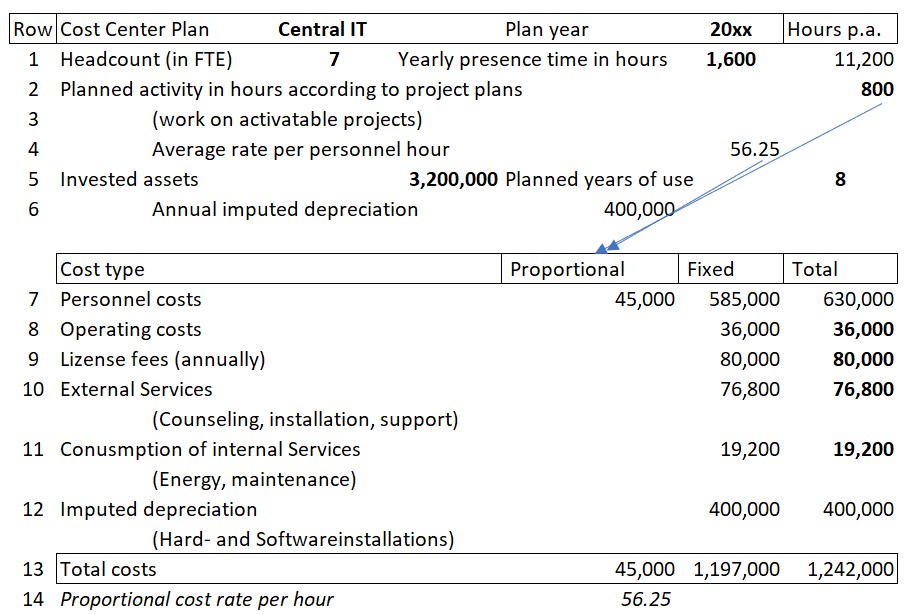

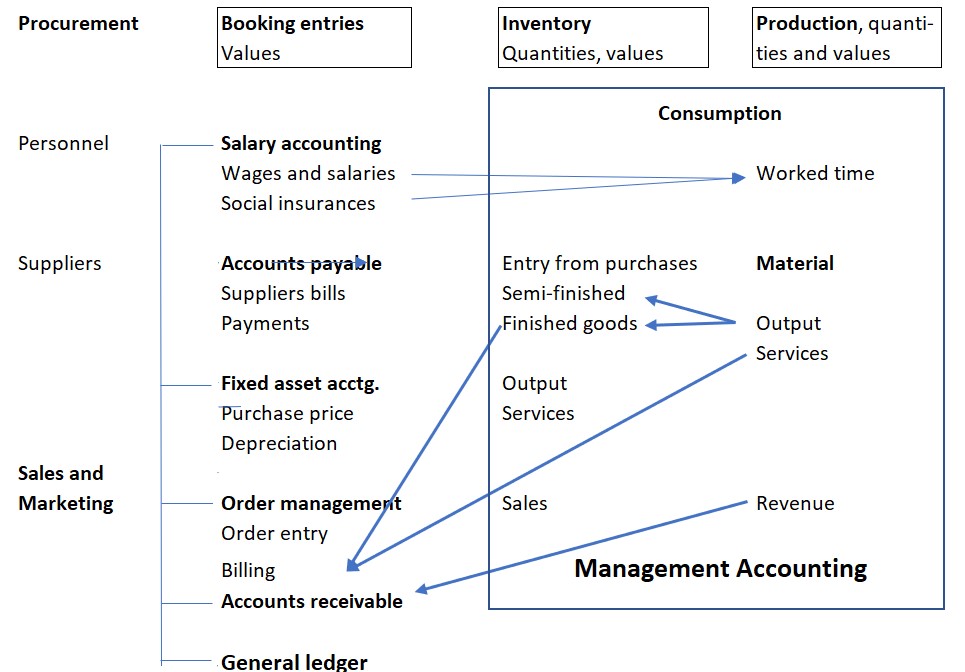

The company’s IT department is responsible for the installation, operation and further development of all applications used throughout the company. In the example company these are: ERP (production planning and control, purchasing and inventories, projects), PLM (product life cycle management), CMS (customer acquisition and support, quotation preparation and tracking, sales orders, analyses), payroll administration, financial and management accounting, internal and external communication (mail, internet presence).

In most cases, several functional areas of a company use these applications. They collect data, analyze content and create evaluations.

The IT department is responsible for the operation, extension and maintenance of the existing applications as well as for the necessary hardware and communication installations. It is also planned that its employees will work 800 hours in the planning year on development projects that can be capitalized and amortized in subsequent years.

For this purpose 7 employees (full-time positions FTE) are employed: (1 IT manager, 4 persons to operate the applications, create evaluations and maintain the hardware and software installations, 2 persons to further develop the applications and work on (capitalizable) projects.

The following cost center plan was defined for the planning year:

Planning the Central IT-Cost Center

Notes:

If the plan is approved as presented, the head of IT is responsible for adhering to the planned costs of 1,242,000 (line 13).

If IT department services were directly dependent on the actual performance of the receiving cost centers, they would have to be charged to the receiving areas at proportional costs. However, there is rarely a direct cause/effect relationship between the recipient’s activities and those of the IT department.

If the costs of further IT developments are to be capitalized, i.e. written to fixed assets, the proportional personnel costs (45,000, line 13) are included because these directly performance-related costs are causally necessary for the creation of fixed assets. All other cost types of the IT cost center are not directly caused by the IT services purchased. They are period costs.

The calculation of imputed annual depreciation in accordance with lines 5 and 12 depends mainly on the valuation rules applied in the respective company (what is capitalized and what is charged directly to the annual financial statements?)

The IT cost center performs various internal tasks. The costs incurred for these are to be planned and accounted for in this cost center.

Conclusion:

Cost planning and the control of internal tasks take place in the cost centers that perform them, because this is where the personnel and systems work, but their costs can rarely be clearly assigned to an individual internal task.

Internal tasks generate period-related fixed costs. This is because their amount is only indirectly dependent on the services produced or sold. Consequently, the costs of internal tasks cannot be charged to the cost centers consuming them or even to the units produced. They are the result of the company’s willingness to perform and the associated management decisions.

Internal tasks can rarely be measured in units, as they usually comprise a bundle of tasks and are not directly related to sales or production quantities.

The costs of an Internal task can usually only be estimated as often several cost centers contribute to an Internal task. However, it is important to continuously record the working time consumption per Internal task. This is because personnel costs carry the most weight and cause the readiness to perform costs to swell.

The costs of all Internal tasks must be covered by the contribution margins.

In the glossary Internal Tasks are defined as “all work performed in the cost centers that is neither directly caused by the quantity of products manufactured and sold nor requested by other cost centers directly depending on their own output”. The post “Internal tasks” in the Management Control blog lists the types of tasks that count as Internal tasks.

The fulfillment of these tasks leads to readiness to perform costs (fixed costs). They are incurred so that production and sales can take place at all. The fixed costs are incurred in the cost centers, but cannot be allocated to products and services according to cause. Readiness to perform costs are planned and approved by the managers. Consequently, the cost center managers and their superiors are also responsible for their amount.

Cost planning for Internal tasks

Cost center budgets must be prepared so that the costs of internal tasks can be assessed and approved for implementation. This requires the following considerations:

1. Time requirements, time consumption of cost center employees per internal task and year, planned services for project orders, time required for cost center management and further training, training.

2. Costs and usage licenses to be paid externally, per internal task or cost center

3. Services from other companies, external costs to fulfill the internal task

4. Services from other cost centers, genuine internal services, e.g. from energy, maintenance, repair, laboratory, transport or IT cost centers (ordered and measurable).

5. Investments and resulting imputed depreciation, acquisition of machinery, equipment, hardware and software; management decision for the planned useful life, calculation of annual imputed depreciation.

The procedure to plan costs for internal tasks is shown in detail in the post “Planning the costs of the central IT-department”.

Decision-making and responsible management accounting require that variances from plan are reported where they occurred. This is where corrective actions must first be determined and implemented if the targeted result is to be achieved (see the post “Management Cycle“). This can be achieved if all stock receipts and issues are valued at proportional planned production costs and if the cost center activities are only passed on to products and other cost centers valued at the proportional planned cost rate.

The following rules must be observed:

All purchased material is valued at the planned purchase price (according to annual planning) during the entire year at warehouse entry or exit

The difference between the planned purchase price and the actual price paid is disclosed as a purchase price variance in the monthly reporting and can thus also be reported on time in financial accounting. Purchasing is responsible for this.

Withdrawals from stock of raw materials and supplies are also debited to the production orders and the consuming cost centers at planned purchase prices Purchase price variances remain with Purchasing.

Manufactured semi-finished and finished products are valuated at proportional planned production costs of the respective item at the time of stock receipt (variances remain in the production orders or in the cost centers performing the work).

Fixed costs are period costs and consequently cannot be allocated to an individual manufactured unit according to the cause.

Stock withdrawals of semi-finished products for processing in further production stages are valuated at proportional planned production costs, i.e. at standard. This is because any variances were already disclosed in the preliminary stage.

Stock withdrawals for sales are also made at proportional planned production costs of finished products (variances were already disclosed in the semi-finished products and in the cost centers). In addition, the sales department is rarely responsible for production variances.

This consistent passing on of the services rendered at proportional production costs or at proportional planned cost rates of the cost centers shows all variances from the plan or from the flexible budget where they originally occurred. This is where corrective actions mainly must be found. The respective managers always have the comparison available between the services rendered at standard and the costs for which they are responsible. Variances from preliminary stages remain there because they also have to be eliminated there. All production and cost center managers can thus assess whether they have complied with their planned costs, taking into account the actual activities performed. This is because they are responsible for the costs they can influence directly.

At the turn of the year, the planned purchase prices and the proportional planned costs of the following year must be applied. This is because the processes and thus the production costs can change in the cost centers and other purchase prices must be provided. Although this requires a revaluation of inventories at the beginning of the year (can largely be automated), it also produces the figures in the following year to be able to present target to actual comparisons relevant for decision-making.

Accounting for Management means providing all managers with the systems and data to enable them to plan and control in a target-oriented manner in their area of responsibility and for the company as a whole. The focus is always on decision-relevant internal reporting and the successful management of the individual divisions.

What about external reporting?

The decision and responsibility-based approach pursued here often does not comply with the valuation rules of accounting standards such as IFRS, US GAAP or national tax law requirements. These rules mostly require the presentation of results in the form of full cost accounting and an externally oriented valuation of inventories.

We compiled the legally binding rules and analyzed their impact on the design of corporate accounting for many countries. In particular, we wanted to know whether legal requirements or accounting standards prohibit or prevent the design of a management accounting system that is uncompromisingly focused on decision making and internal accountability.

This analysis was revised and updated several times. Download the 2019 version with the link below (sorry, until now only available in German): Lukas Rieder, Markus Berger-Vogel: “Fixed Cost Allocations: one or none?”

Here we anticipate the key findings from this analysis:

There are no statutory accounting requirements or international reporting standards that prohibit or otherwise prescribe the structure of the decision- and responsibility-driven management isaccounting system recommended in this blog.

In management accounting, the starting points are the individual item, the processes and cost centers and the people working in them. These elements must be planned and controlled in detail if a company is to remain successful in the long term. Evaluations are mostly condensations on higher observation levels, which deny the view of the control-relevant details.

With reference to the valuation of inventories and thus the determination of the externally reported annual result, it makes sense to always value all inventory receipts and issues at proportional planned production costs. It is easy to adjust inventory valuations to accounting rules in an automated side-by-side calculation to generate external reports. However, financial success is generated in the market and internally, not through external reporting.

Cost price is the total cost of a company in a period, adjusted for changes in inventory. According to Wikipedia.org, this includes material costs, manufacturing costs, research and development costs, administrative costs and distribution costs. as well as imputed interest for assets required for operations (see German Guidelines for Price Determination on the Basis of Cost of Goods Sold (Annex to Regulation PR No. 30/53 of November 21, 1953, Notes 43 – 45)). If the net revenues exceed the cost price, the company starts to make a profit.

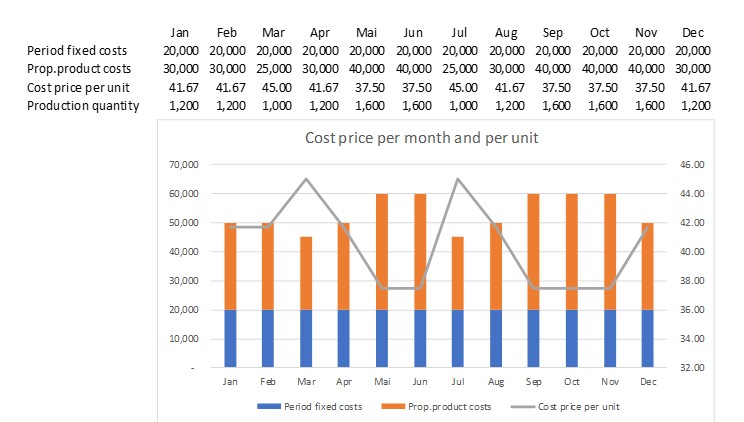

This statement is true for the company as a whole but it misleads when it comes to management control. Who wants to calculate the cost price of an article, a customer or a subdivision of the company, has to break down the fixed costs to product units. But as there is no direct cause-and-effect relationship between the company’s fixed costs and the individual product unit sold, this can never be done properly

To calculate the profit contribution of an item, the cost price per unit of a product or service unit sold must be calculated. All fixed period costs must therefore be allocated to the product units sold. For this purpose, an overhead rate is determined for the calculation of the unit cost of goods sold. If the sales quantities or the fixed cost blocks change, the cost price per unit unit also changes. This affects inventory valuation and, even more important, the management of sales and production.

As long as neither the bill of materials nor the routing and neither the material purchase prices nor the proportional planned cost rates of the cost centers involved in production change, the proportional costs incurred per unit produced remain the same. However, distributing the fixed costs to a different production or sales quantity, results in different cost prices per unit. Neither production nor sales are responsible for this, only the capacity utilization.

Cost price is irrelevant for descision-making

In the example, the monthly cost price per unit of goods sold changes because the fixed costs are divided by the production quantity of the period under review. If inventory receipts and issues are valued monthly at full productions costs, they include a portion of the period’s fixed costs. The value per unit thus changes every month. The fixed costs of other functional areas of a company are usually added as percentages to the full production costs. Although cost of goods sold is necessary in external reporting, it is not useful for corporate management purposes:

If the really paid purchase prices deviate from the planned ones, first the purchasing department is responsible for the variances.

If in the production processes more direct material is consumed per unit produced than planned (or more semi-finished products), the production management is responsible.

If the standard times for the manufactured product units are not adhered to in the production cost centers, it is up to the respective cost center managers to take corrective action.

The data required for this can only be obtained if the splitting into proportional and fixed costs has been set up in the management accounting system. This can be achieved with marginal costing (flexible standard costing), see the posts “Full product costs are always wrong” and “Complete variance analysis“).

Since the demand, respectively the customers and the ability of one’s own sales organization determine the net revenues, it is necessary to compare the latter with the proportional product costs of the services and products sold. Our experience shows that most companies sell their items at different contribution margins per unit. The sum of all contribution margins achieved must be sufficient to cover all fixed costs and the targeted profit. An item that does not cover its calculated cost price can still make a considerable contribution to covering fixed costs.

The aim is always to cover all fixed costs and all variances with the contribution margins from the units sold, while at the same time achieving a profit in line with the market.

Management Accounting is a Prerequisite for Financial Accounting

Many companies base their choice of software modules to be used for ERP and accounting on legal requirements. Financial accounting must be kept because profit or loss as well as assets and liabilities must be reported at least once a year. At the same time, accounting regulations must be complied with (local commercial and tax law, internal settlements between companies of a group).

In addition, the rules of the international accounting standards (IFRS, US GAAP and the like) mostly assume the following basic structure of the income statement:

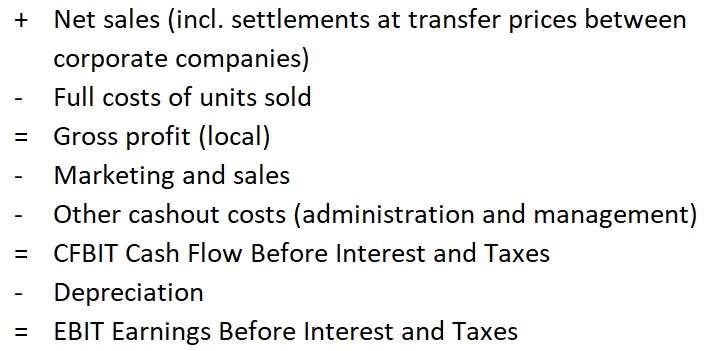

Full cost structure of the profit and loss account

This is the usual form of the profit and loss account presented externally and very often internally. It can be created with auxiliary calculations from financial accounting. All consumptions incurred in a period for the plant (material, personnel, external services, depreciation and even pro rata interest costs) are debited to the plant cost center (simplified all costs incurred within the fence of the plant). This results in the full cost of goods sold after accrual of inventory changes. Similarly, all marketing and sales costs are concentrated in the collective cost center for marketing and sales. Also, the costs for administration and management and possibly for research and development are added as a percentage of the full costs of products sold. This presentation mostly meets the requirements of the mentioned external standards of financial accounting.

However, the executives of a company, especially the product and cost center managers plan and decide quantities, activities and prices and create new products and services by means of input factors such as working time, material or energy. Corporate management expects all managers of lower levels to take responsibility for the costs of their area. To this end, it must be ensured that there is a causation-based relationship between costs and the units created and sold.

Cost, performance, revenue and profitability accounting

The relationship to quantities, consumption and values can only be established in a management accounting that presents cost, activity, revenue and earnings. This system calculates how much the consumed quantities and services did or should have cost per product or service unit. Accounting for management is a matter of calculating the plan, target and actual of the units produced and sold. Because both the cost and the revenue side are included, the term management accounting became established.

The figure below shows that in the various auxiliary accounts and in the summarizing general ledger accounting, the focus is on the period view for the company. In the right-hand management accounting section, on the other hand, the order or unit view is decisive. Managers at all levels want to know how much it cost to manufacture a product or service unit in their management area. In order to calculate the result for the period, it must also be known by how much the inventory quantities of raw materials, semi-finished and finished products have changed per item. Costing per product unit is a prerequisite for this valuation.

Data flows order costing

In the accounting-based full cost structure of profitability analysis, both unit and period costs are deducted from net revenues to arrive at Gross Profit. Example:

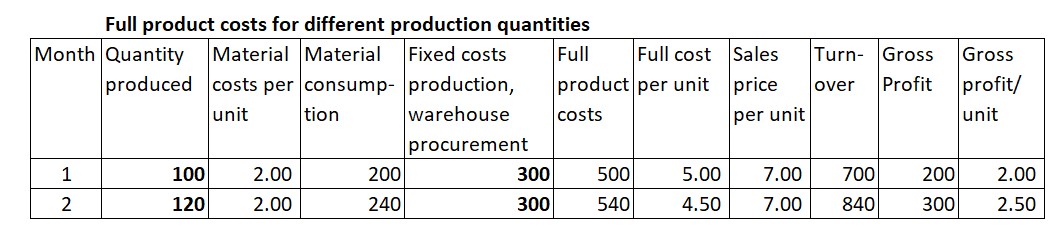

Full product costs per unit

In month 1,100 pieces were produced and sold. This resulted in full production costs of 500, taking into account the cost center costs of production,warehousing and purchasing. In month 2, 120 pieces were produced and sold at the same material purchase price of 2.00 per piece. According to accounting, the personnel costs remained at 300 (the existing employees had enough capacity for the additional production). As a result, the full manufacturing cost per piece dropped from 5.00 to 4.50.

Questions:

Is the finished goods inventory receipt to be posted at a different valuation each month (moving average)?

If yes, does the gross profit per unit change each month because the capacity utilization is different? What is the correct valuation approach for planning and managing sales?

The differing full costs of goods sold per unit are the result of the utilization of the production cost centers. The staffing and machinery of these cost centers is determined by production managers, not by sales.

Planned and actual costing are core functions of management accounting.

The calculated values are not only used for inventory valuation but above all are compared with the net revenues generated by sales. As the sales organization is not responsible for variances in production and procurement this requires that direct material consumption is valued at planned purchase prices and work plan positions are valued at the planned proportional cost rates of the cost centers. Splitting cost center costs into their proportional part (driven by the products) and their fixed part (driven by the dimensions of the cost centers) is a key requirement for decision-relevance.

Controllers and management accountants must therefore set up their system in such a way that a distinction can already be made in the standard cost estimate between proportional costs directly caused by the products manufactured and fixed costs that are mainly the result of management decisions. This is because the net revenue from a sale to a customer must first be compared with those costs that can be allocated to this order in a manner that reflects their cause. In the absence of a direct cause-and-effect relationship, fixed costs can only be allocated to a product or a customer by applying allocation keys that are arbitrarily chosen by the majority. Only small proportions of marketing and selling costs and other cash out costs can be allocated to an individual product or customer on the basis of causation.

In Accounting for Management rules such as IFRS, US GAAP or tax laws do not apply. They lead to incorrect decisions.

Example: A product with a high proportion of material or external activity costs must bear a higher proportion of the fixed costs of purchasing and the warehouse cost centers, even if its procurement is uncomplicated and can be handled with a telephone call or an e-mail. This increases the full manufacturing costs of this product, with the result that the markups for marketing and sales costs and for other cash costs and depreciation also increase. This is because such surcharges are calculated on the basis of the full manufacturing costs. The product then no longer looks particularly worthy of promotion because it is “broken” by surcharges.

Conclusion: A management accounting system is built to support all managers of a company in their decision-making so that they can achieve an overall improvement in the company’s results. Fixed cost allocation does not help in this optimization process. According to the current state of knowledge, it is recommended to set up management accounting as marginal costing, combined with multi-level contribution margin accounting .

The Institute for Management Accounting IMA still trains and propagates the “full cost structure of profit and loss accounting”. The focus is still on external reporting, not on internal decision making. These non-decision-making guidelines led to the establishment of the Profitability Analytics Center of Excellence (PACE). Find practical examples and technical papers on how management accounting can increasingly fulfill its mandate to show executives ways to improve results on their homepage.

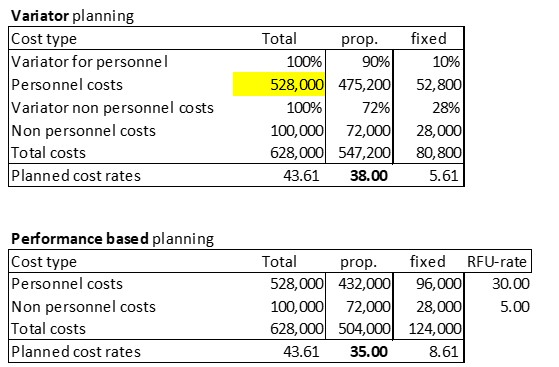

In many textbooks and partly also in cost accounting software the variator method is recommended to split cost center costs into their proportional and their fixed part. The planned proportional costs are given as a percentage of the planned costs of a cost type in a cost center and the complement is the fixed costs of this cost type. Using variators for cost splitting should be omitted because it generates incorrect cost rates. The example explains this:

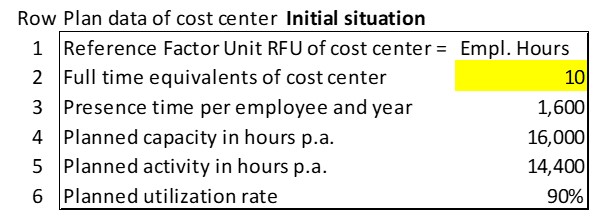

Initial situation in annual planning

The annual production plan shows that the cost center to be planned should work 14,400 hours on production orders. The cost center manager plans, including himself, a staff of 10 persons, each working 1,600 hours per year. The planned yearly personnel costs will amount to 480,000 EUR, the average rate per presence-hour and employee thus to 30.00 EUR. 90% of the planned 16,000 presence time hours are to be used for manufacturing (14,400 hours) and 10% for organization ant training. Thus the variator of 90% results (row 6).

Variators for cost splitting

The planned non-personnel costs (including depreciation) amount to 100,000, of which it is estimated that 5.00 are to be used per hour of planned employment. This corresponds to proportional non personnel costs of 72,000 and thus a variator-rate of 72% (rows 9 and 10).

Initial variator

Comparing the variator method and direct activity-based planning shows (still) the same planned cost rates, e.g. 35.00 proportional hourly cost rate.

But the executives and the cost center manager expect stronger fluctuations of the production quantities in the plan year. They decide to equip the cost center with an eleventh employee (security variant). This increases the installed capacity to 17,600 hours and the planned personnel costs to 528,000. But the planned employment remains at 14,400 hours per year. Due to the variator of 90% the higher personnel costs raise the proportional hourly rate from 35.00 to 38.00, although the same number of hours is worked for the products to be manufactured.

Increased employee-capacity

It is the fixed cost-rate that has to change from 5.61 to 8.61 as more fixed costs are included in the products. The proportional planned costs per unit remain the same. This is appropriate, since the costs of the additional employee only become proportional costs when his hours are used for manufacturing.

Variators belong to the master data of cost accounting and it is not intended that they be adjusted by cost element each time there is a change in normal capacity or planned employment. The variant with 11 employees results in incorrect cost rates. This is because also in the second variant, 30.00 personnel costs and 5.00 material costs are incurred for each hour worked on order; it is the same people with the same wages who perform this work. If, as a result of a revised sales plan, plan employment were increased, each variator would also have to be adjusted.

If in the subsequent plan year, non-personnel costs increase from 100,000 to 120,000 because fixed depreciation and non-personnel costs increase, a portion of the fixed costs will be “shifted” to the proportional plan cost rate if the 72% variator remains the same. As a result, period fixed costs are understated.

Conclusion: Variators are unsuitable for the design of a flexible budget costing and a real contribution margin accounting. They have to be adjusted cost type by cost type in the master data with every activity change. Flexible budgeting produces the correct values. In addition, it ensures that the proportional planned cost rate remains the same even with changes in the production program and thus with other planned activities.

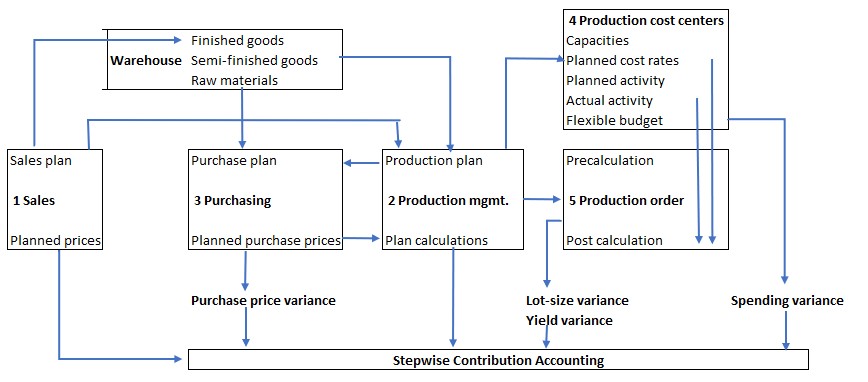

Product costing follows the planning and control process of a company:

In sales, the quantity-based annual sales plan is drawn up per finished item, be it a physical product or a service unit.

Production management determines the quantities to be produced per item on the basis of the sales plan. In doing so, it takes into account the existing inventory, the machine and personnel capacities of the production cost centers as well as expected interruption times due to vacations, public holidays and machine maintenance. Production management wants to have enough semi-finished products in inventory at all times in order to deliver the units sold on time and still manage with minimum average inventory levels. Therefore, production management must determine the lot sizes of the individual production orders.

Purchasing ensures that the material requirements resulting from production and sales planning are available in stock on time. In addition, it negotiates with the potential suppliers in good time the planned purchase prices of the products and services to be bought. This is necessary to calculate the planned costs of the products and services.

The managers of the manufacturing cost centers prepare the planning of their cost center on the basis of the planned activities resulting from the production plan. To do this, they need the planned production quantities, the standard times from the work plans for the items they produce and the setup-times to be scheduled for each production order. With this information they determine the planned activity of their cost center, i.e. the activity that is to be performed directly for the production orders to be processed.In the next step, the cost center managers consider how much auxiliary or operating materials will be required from the warehouse or directly from the suppliers in order to be able to perform the planned activity. They also plan which services will have to be procured from internal auxiliary cost centers (e.g. energy, water, compressed air, repairs and maintenance) depending on the planned employment.

Target and Actual of Production Orders

The sum of these planned costs is divided by the planned activity, which results in the proportional planned cost rate of the cost center. This rate is used for the calculation of proportional product costs in planning as well as in actual (5). This data can be used to calculate the planned proportional (standard) costs of an item and the precalculation of a real production order. If these are deducted fromnet sales, the contribution margin I per product and summarized per product or customer group can be calculated, also in planned and actual data.

The precalculations of the orders of a month are decisive for the calculation of the monthly flexible budgets of the production cost centers. If the actual costs deviate from the flexible budget, consumption variances arise (per cost element). The cost center manager is responsible for these. He must ensure that corrections are made so that the company can achieve its profit targets.

Only a few variance types can clearly be assigned to the individual production order:

A lot size variance occurs when the production lots ordered deviate from the planned lot size in the annual plan. If the quantity ordered in a production order is larger than the quantity planned in the standard cost estimate for the article in question, the setup costs are spread over more units. As a result, the item produced costs slightly less per unit.

Yield variances occur when more or fewer “good quality” pieces result from the production order than planned. This happens primarily in process manufacturing, e.g. in the production of chips for processors or in chemical processes.

Material quantity variances occur when the input material did not fully meet the specifications or when the processing machines were not precisely adjusted. They lead to cost overruns in the respective production order.

Work time variances occur in the cost centers of production when more or less process time has been used than in the plan-calculation of the order. These over- or under-consumptions can be assigned to the individual order if the processing cost centers record their output per order.

Purchase price variances occur when the really price paid for raw materials and purchased services does not correspond to the planned price (especially in the case of inflation). They can be calculated in purchasing when the supplier invoice is recorded. Because the purchasing department negotiates the contracts with the suppliers, it is also responsible for purchase price variances.

As the same material can be used for different products and in many production orders, most purchase price variances can neither be assigned to an individual production order nor to a cost center according to cause. Direct assignment is only possible when materials or services are procured directly for a production order or a cost center.

Usually, raw materials and supplies are first stored in inventory and are only assigned to the production orders or cost centers when they are taken from the warehouse (material withdrawal slip). If actual purchase prices are used to value the inventory, the same material is in stock at different purchase prices. As a result, production would encounter a different average purchase price for the material each time they use this material.

If the production orders are debited according to the first in – first out principle, the order processed earlier still benefits from the lower-priced material, while the subsequent order is charged the higher prices. Valuing inventories with moving average prices does not help either. This is because each production order delivered to inventory results in new (proportional) unit costs and thus different valuation approaches in the warehouse for the same finished item.

If all warehouse receipts and issues are valued at standard purchase prices, this dilemma can be avoided. Production and sales can then (internally) purchase the materials throughout the year at the standard purchase price, and purchasing can determine the purchase price variance at the moment of purchase, i.e. when it occurs.

In the cost centers, the flexible budget costs, i.e. the planned costs of the actual activity performed, must be adhered to. The cost center managers are responsible to avoid negative differences between target and actual costs, i.e. spending variances, and for ensuring that these variances disappear in subsequent periods.

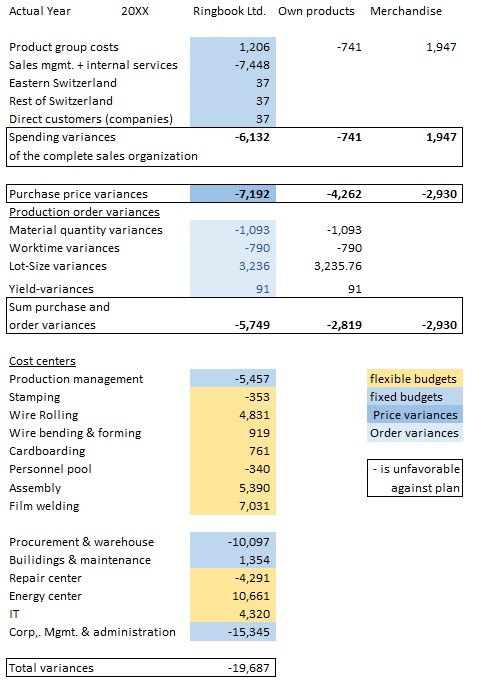

The example below has already been presented in a similar form in the post “Complete variance analysis“. All variances from the target are presented at the lowest hierarchical level to which they can be clearly assigned. This is also the place to intervene if these variances are to be avoided in the future.

Different types of variances

This illustration only shows internal variances within the company. Changes in net sales are analyzed in contribution accounting.

Initial situation: In the annual plan derived from strategy and medium-term plans, it is determined which items (services or physical products) are to be manufactured at what cost. For this purpose, the planned proportional production costs per unit are to be calculated in the costing system. In the sense of Management by Objectives the responsible persons have the task of adhering to these planned proportional product costs in each production order. This requires that each responsible person (e.g., production managers and project managers) must be able to track which costs were directly caused by an order. This is because they can only take responsibility for the cost elements that they can directly influence.

Three types of costing are distinguished because they serve different purposes:

Standard costing: Determination of the planned costs of a unit of an item (physical product or service) as part of annual planning. This costing results in the (annual) planned costs per unit produced.

Precalculation: On the basis of the planned costs and the actual quantities ordered, the planned costs of an order to be actually executed are calculated. This is because the actual incoming orders rarely match the planned quantities. Precalculation forms the basis for the target to actual comparison of a production order that has been placed.

Post-calculation: Comparison of the costs incurred in the actual order compared to the precalculation.

With this target to actual comparison managers are enabled to identify the order items that have deviated from the plan. With this information they can intervene in the next periods and find measures that will lead to achieving the target costs again in the following periods. In addition, it must be ensured that cost variances are not passed on to subsequent levels. This is because these are only responsible for their own variances.

Cost center-managers as well as production- and project-managers are responsible for variances in the production area. In decision-relevant management accounting the variances of production and all cost centers should not be charged on, neither to the warehouse nor to the sales organization, since the latter cannot be responsible for such variances. For management-relevant Profitability Analysis (step-by-step contribution accounting), it follows that during the year all warehouse receipts should be valuated at proportional planned production costs and the variances should be shown in the (monthly) Profitability Analysis. This is because the variance types mentioned can neither be allocated to the products nor to the sales organization nor to the individual customers according to their cause.

The next two posts show how the various types of variances are shown in Profitability Analysis in a way that is appropriate to the levels and responsibilities, where they are to be shown, and how inventories are to be valued.