Projects cause investments and costs. These are to be included in management accounting in order to present the complete result. The necessary data is presented here.

Project cost planning

To release a project order its financial effects should be determined as well. Project cost planning requires a similar procedure as for product costing. As projects also generate costs and investments they also have to be represented in the management accounting system.

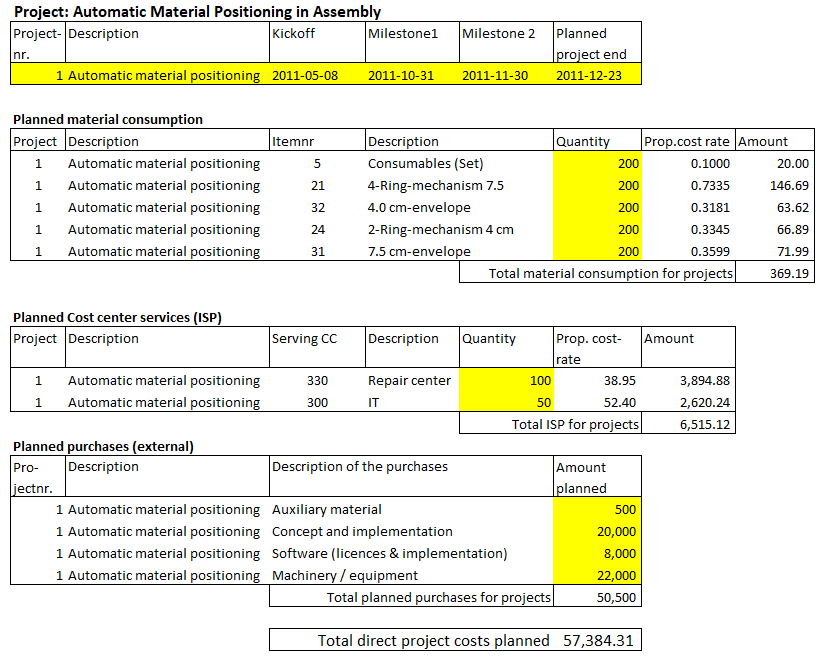

In the assembly cost center of the example company the material positioning (envelope and mechanism) should be automated with the help of a loading robot and at the same time enable an accurate positioning of the parts. Manager of this project is the head of the Assembly cost center. His employees will help set up the equipment and test it. An external company will be commissioned to handle the project, the in-house maintenance and repair center will ensure the availability of compressed air and electricity, and the in-house IT department will program and test the interfaces for the transmission of production order data.

The same procedure as for the manufacture of a product should therefore be provided for:

Material consumption for testing

Internal services of the cost centers Maintenance and Repairs and IT

The time needed in the Assembly department to put the installation into operation (internal tasks)

The external expenditures for the system (including installation) for testing (third-party invoices, cash out).

The internal services provided are already included in the post “Planning the Internal Services Provided”. These services, the investment, and the material consumption will be posted to the balance sheet as assets under construction. This is recommended from a management perspective, because the costs of the investment will not appear as (imputed) depreciation in the assembly cost center until the following periods. The points to be considered when determining depreciation in Management Accounting are discussed in another post.

Because projects will soon be omnipresent in companies, the working time requirements for internal tasks and for internal services provided in particular must be planned in detail. These hours have an increasing impact on personnel requirements planning.

Cost center planning begins with clarifying which production-dependent activities are to be performed in the plan period and which additional internal tasks are to be performed. This activity reference forms the basis for determining the planned costs per cost element.

Plan Cost Centers

Quantity, activity, and task-related annual planning as described in previous posts generate the orders for the cost center managers responsible for implementation. Like every manager, they are responsible in their area for QQDR: qualities, quantities, dates, and results (see the post “The management cycle determines the value types”). The performance requirements arise from:

the planned production quantities envisaged,

the necessary internal services provided, and

the planned internal tasks.

As a first step, cost center managers must therefore consider what services or results their area must deliver. From this, it can then be derived which staffing levels and which assets are required for this. The requirements are derived from the plans already drawn up:

From the planned production quantities, the planned activity levels of a production cost center can be derived with the help of the work plans. From this, the personnel requirements for the production-related work are determined.

From the internal tasks planned for the given cost center, the hourly requirements for work that is not directly production-related are derived. These are the working times for cost center management, training and education, inspection work, participation in projects, and attendance at meetings of all types.

The machines and installations installed in a cost center largely determine how much activity will have to be obtained from internal service providers (workshops, maintenance, internal transportation, energy, and so on).

The head of the Stamping cost center has the following planning basis concerning activities, employees, and machinery:

According to production planning, his cost center should be ready for an activity level of 338,855 personnel minutes (Pmin).

For the stamping work and for internal tasks, 4 full-time positions are required (including the manager), as each employee is planned with a net annual presence time (vacation public holidays and other absences already deducted) of 102,000 minutes (4 x 102,000 = 408,000 minutes).

The capacity of the installed machines is still sufficient at 435,840 minutes.

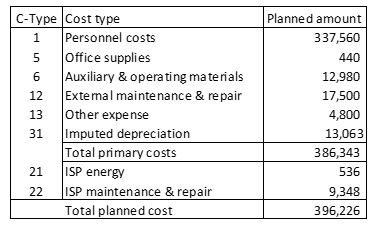

On this basis, he begins to plan the primary costs to be incurred for the planned activity. To do this, he receives a list of the plannable cost types from the controller. This is shorter than the list of the expense types in accounting as it is defined to plan the costs of this cost centers consumption:

To do this, the personnel costs including all social welfare costs are prepared in the personnel area and reported to the cost center manager as a total amount. Since the cost center manager cannot change the rates for additional wage-dependent costs (for example, insurance, vacation), one aggregate cost category for Personnel costs is sufficient. This makes planning and control easier.

The controller prepares the imputed depreciation amounts in Fixed Asset Accounting based on the assets installed in each cost center and reports this information to the cost center manager.

Primary costs are characterized by the fact that they come from outside the company and, with few exceptions, are always posted in Accounts Payable or Payroll Accounting. If such costs are to be provided in the cost center (office materials, supplies, etc.), the planner consults invoices from previous years, maintenance plans and other documents to determine the planned cost amount.

This procedure is directly linked to the process of management by objectives. Once the cost center manager has prepared his cost and activity planning, he agrees on the target cost center budget with his boss. For this reason, the cost center plan may only contain amounts and cost elements that the responsible person can influence directly.

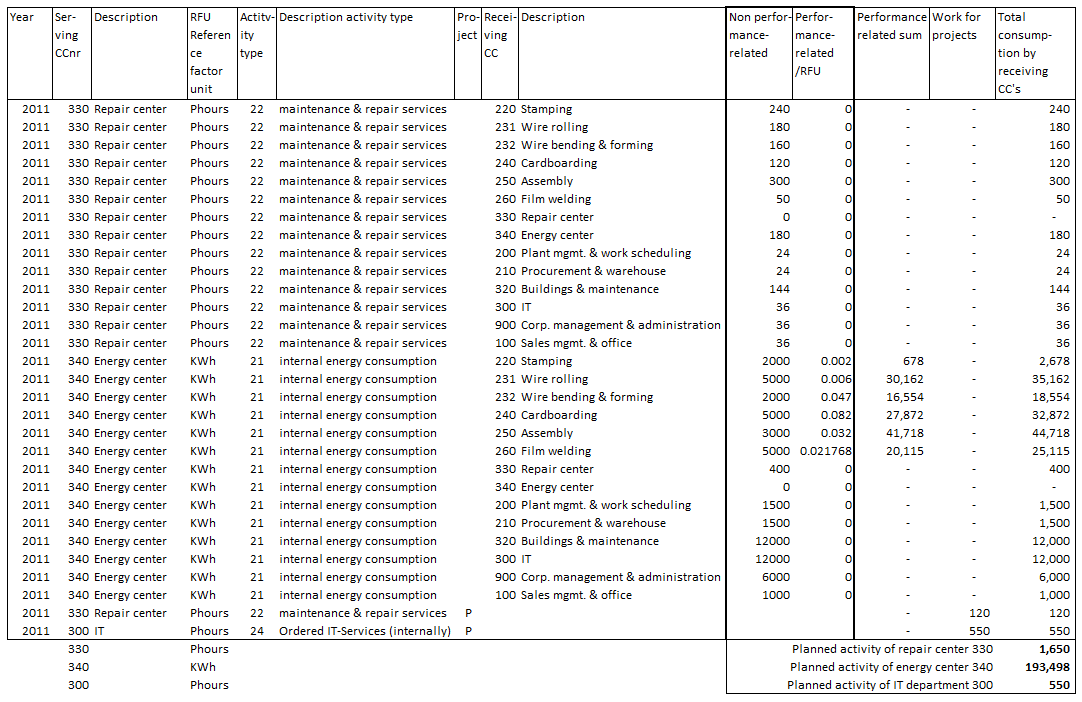

Cost center planning does not yet contain the planned costs for internal services provided. These are called secondary costs as they stem from another cost center. In the table of planned internal activities in the post “internal services provided” it was shown that in the plan year 240 service-hours are to be obtained from the maintenance and repairs cost center (330). Its hourly rate is 38.95, which results in a debit of 9,348. The planned cost for energy consumption was calculated accordingly. A total of 536 is planned for this. The complete planned costs of the stamping shop are as follows:

We speak of Internal Services Provided if a service from another cost center is explicitly ordered by the receiving cost center or if the service is directly caused by the activity of this cost center. For Internal Tasks no order exists. This is why they cannot be charged according to the cause to other cost centers. But for Internal Services Provided the direct causation link exists. This why the latter can be charged to the receiving cost centers but not the internal tasks.

Plan Internal Services to be provided

Internal services are provided when a receiving cost center directly orders services (activities) from another cost center. Such an order can be placed explicitly or be the direct consequence of the activity level of the ordering cost center. The supplying area is therefore responsible for providing the service.

Examples:

A car of the sales department is damaged and repaired in the company’s own garage (the order could also have been placed externally).

Every 100 operating hours the repair department has to check the dimensional accuracy of the rolls in the Rolling and Punching cost center for four hours and replace the rolls if necessary.

The maintenance group receives an order to rebuild the entrance of the reception building according to the latest safety standards.

The energy supply division supplies all other divisions of the company with electricity, water, and compressed air. Consumption is directly dependent on the equipment installations and on the performance of the receiving cost centers. It can be measured using meters or calculated using consumption tables.

Every tenth production order must be checked in the internal laboratory for compliance with all quality regulations.

In these cases, the ordering cost center is the trigger for the production of the service, either through an explicit order or through an automatic relationship between the service provided in the ordering area and the service delivered by the service area (2,4,5 above). The originator of the service procurement is always the delivering party. The ordering party should plan (in cooperation with the internal supplier) the services for a year, so that the personnel and machine capacities required by the internal supplier can be determined from this information.

In the example company Ringbook Ltd., the genuine internal exchange of services is planned in the following table:

All planned internal services

The consumption estimates of the receiving cost centers are collected and converted to the personnel hours or kWh required. A distinction must be made between which consumption is dependent of the activities of the receiving cost centers and which is independent (mainly calendar-driven). Totaling the values in the last column gives the planned activity levels of the internal service providers.

The purpose of Management Accounting is to support all managers in decision-making and responsibility taking.

Planning and control instruments must be management oriented in order to be relevant for decision-making. The purpose of Management Accounting is to support management. Information provided by the system should be presented in a planning and control-compliant manner up to the balance sheet, so that managers can plan and control their areas of responsibility and coordinate them mutually.

The Focus of Management Accounting

The focus is always on the self-reliant management of a given area. Customers, sales, products, cost centers and projects are in the center. For a cost center the following questions arise:

Which and how many activity units should we provide and what should be their performance-related costs (planning of proportional costs)?

Which structures must be available to be ready to generate the requested output and how much should these cost (planning of fixed costs)?

What was the actual activity level in a given period of time and how much should this perfomance have cost (flexible budget of the actual performance)?

Which costs directly attributable to our area have actually been incurred (actual cost recording)?

What differences between the flexible budget and actual costs have arisen for which we are responsible (variance analysis)?

What further development do we expect by the end of the year or project, taking into account what has been achieved and the corrective measures already planned (forecast)?

Overall, Accounting for Management is a support for decision-making in planning, implementation, control, correction and expectation (i.e., the management cycle). This requires the inclusion of services, revenues and inventories, represented in quantities and values. A consistently designed management-oriented activity, cost, revenue and profit accounting system that can represent plan, target, actual and forecast is a prerequisite. The underlying data comes from the dispositional systems (ERP) and from the accounting system.

Controllers are responsible for the design, implementation and operation of this overall system.

Valuation requirements from laws and accounting standards are of secondary importance for the design of Management Accounting, because internal and market-related planning and control are the main focus.

Accounting for Management can only do justice to its purpose if it shows the person responsible in each case the variables in plan, target, actual and forecast that can be directly influenced by him and his employees.