Management&Controlling&Controller

Management Control is defined as the process by which managers at all hierarchical levels ensure that their (strategic) intentions are realized.

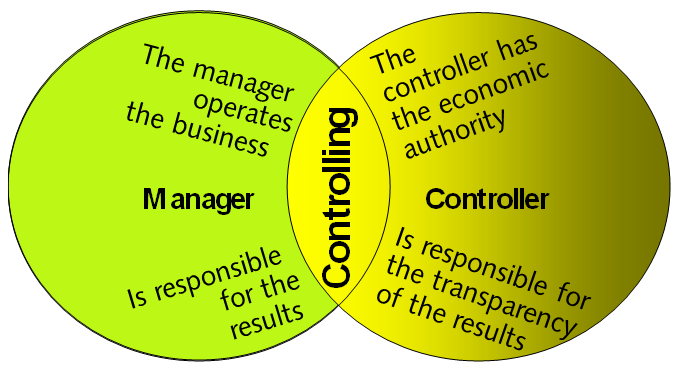

Managers do the controlling, controllers empower them to do so. Controllers are enablers. “As management partners controllers make a significant contribution to the sustainable success of the organization” See the controller mission statement of the International Group of Controlling (IGC) and of the International Controller Association (ICV). “Controllers

-

- design and accompany the management process of goal fixing, planning and controlling, so that every decision-maker can act in an objective-oriented manner,

- ensure the conscious preoccupation with the future and thus make it possible to take advantage of opportunities and manage risks,

- integrate an organization‘s goals and plans into a cohesive whole,

- develop and maintain all management control systems. They ensure the quality of data and provide decision-relevant information,

- are the economic conscience and thus committed to the good of an organization as a whole.” See https://www.igc-controlling.org/“

Controllers are thus responsible for the design, operation and content of the management control systems.

Controllers do not practice controlling. Controlling is done by managers when they perform their planning and control tasks. A department with the designation “Controlling” is therefore a contradiction in terms. Controllers work in a controller department or in controller services. This distinction is important to avoid disputes about responsibilities and competencies.

In other words: To prepare the various budgets and to integrate them in the overall plan is the controller’s task. Preparing, approving and releasing budgets is just as much a management task as the realization of the factual and financial objectives.